An Particular person Retirement Account (IRA) is a sort of funding account with tax benefits that helps you put together for retirement. Relying on the kind of IRA you spend money on, you can also make tax-free withdrawals whenever you retire, earn tax-free curiosity, or postpone paying taxes till retirement.

The earlier you begin investing in an IRA, the extra time you need to accrue curiosity earlier than you attain retirement age. However an IRA isn’t the one type of funding account for retirement planning. And there are a number of forms of IRAs obtainable. In the event you’re planning for retirement, it’s vital to know your choices and discover ways to maximize your tax advantages.

In case your employer presents a 401(ok), it could be a greater possibility than investing in an IRA. Whereas anybody can open an IRA, employers sometimes match a portion of your contribution to a 401(ok) account, serving to your funding develop quicker.

On this article, we’ll stroll you thru:

- What makes an IRA totally different from a 401(ok)

- The forms of IRAs

- How to decide on between a Roth IRA and a Conventional IRA

- Timing your IRA contributions

- IRA recharacterizations

- Roth IRA conversions

Let’s begin by taking a look at what makes an Particular person Retirement Account totally different from a 401(ok).

How is an IRA totally different from a 401(ok)?

With regards to retirement planning, the 2 commonest funding accounts individuals speak about are IRAs and 401(ok)s. 401(ok)s provide comparable tax benefits to IRAs, however not everybody has this selection. Anybody can begin an IRA, however a 401(ok) is what’s often known as an employer-sponsored retirement plan. It’s solely obtainable by means of an employer.

Different variations between these two forms of accounts are that:

- Employers usually match a proportion of your contributions to a 401(ok)

- 401(ok) contributions come proper out of your paycheck

- 401(ok) contribution limits are considerably larger

In case your employer matches contributions to a 401(ok), they’re mainly providing you with free cash you wouldn’t in any other case obtain. It’s sometimes clever to benefit from this match earlier than trying to an IRA.

With an Particular person Retirement Account, you establish precisely when and methods to make a contribution. You may put cash into an IRA at any time over the course of the yr, whereas a 401(ok) virtually at all times has to come back out of your paycheck. Be aware that annual IRA contributions will be made up till that yr’s tax submitting deadline, whereas the contribution deadline for 401(ok)s is on the finish of every calendar yr. Studying methods to time your IRA contributions can considerably improve your earnings over time.

Yearly, you’re solely allowed to place a hard and fast amount of cash right into a retirement account, and the precise quantity usually adjustments year-to-year. For an IRA, the contribution restrict for 2024 is $7,000 in the event you’re underneath 50, or $8,000 in the event you’re 50 or older. For a 401(ok), the contribution restrict for 2024 is $23,000 in the event you’re underneath 50, or $30,500 in the event you’re 50 or older. These contribution limits are separate, so it’s not unusual for buyers to have each a 401(ok) and an IRA.

What are the forms of IRAs?

The problem for most individuals trying into IRAs is knowing which type of IRA is most advantageous for them. For a lot of, this boils right down to Roth and/or Conventional. The benefits of every can shift over time as tax legal guidelines and your earnings stage adjustments, so this can be a widespread periodic query for even superior buyers.

As a aspect observe, there are different IRA choices suited to the self-employed or small enterprise proprietor, such because the SEP IRA, however we received’t go into these right here.

As talked about within the part above, IRA contributions will not be made immediately out of your paycheck. That implies that the cash you’re contributing to an IRA has already been taxed. If you contribute to a Conventional IRA, your contribution could also be tax-deductible. Whether or not you’re eligible to take a full, partial, or any deduction in any respect is determined by in the event you or your partner is roofed by an employer retirement plan (i.e. a 401(ok)) and your earnings stage (extra on these limitations later).

As soon as funds are in your Conventional IRA, you’ll not pay any earnings taxes on funding earnings till you start to withdraw from the account. Because of this you profit from “tax-deferred” progress. In the event you have been in a position to deduct your contributions, you’ll pay earnings tax on the contributions in addition to earnings on the time of withdrawal. If you weren’t eligible to take a deduction in your contributions, then you definately typically will solely pay taxes on the earnings on the time of withdrawal. That is performed on a “pro-rata” foundation.

Comparatively, contributions to a Roth IRA will not be tax deductible. When it comes time to withdraw out of your Roth IRA, your withdrawals will typically be tax free—even the curiosity you’ve gathered.

How to decide on between a Roth IRA and a Conventional IRA

For most individuals, selecting an Particular person Retirement Account is a matter of deciding between a Roth IRA and a Conventional IRA. Neither possibility is inherently higher: it is determined by your earnings and your tax bracket now and in retirement.

Your earnings determines whether or not you may contribute to a Roth IRA, and likewise whether or not you’re eligible to deduct contributions made to a Conventional IRA. Nonetheless, the IRS doesn’t use your gross earnings; they have a look at your modified adjusted gross earnings, which will be totally different from taxable earnings. With Roth IRAs, your capacity to contribute is phased out when your modified adjusted gross earnings (MAGI) reaches a sure stage.

In the event you’re eligible for each forms of IRAs, the selection usually comes right down to what tax bracket you’re in now, and what tax bracket you suppose you’ll be in whenever you retire. In the event you suppose you’ll be in a decrease tax bracket whenever you retire, suspending taxes with a Conventional IRA will possible end in you protecting extra of your cash. In the event you count on to be in a better tax bracket whenever you retire, utilizing a Roth IRA to pay taxes now will be the more sensible choice.

One of the best kind of account for it’s possible you’ll change over time, however making a selection now doesn’t lock you into one possibility endlessly. In order you begin retirement planning, give attention to the place you are actually and the place you’d wish to be then. It’s wholesome to re-evaluate your place periodically, particularly whenever you undergo main monetary transitions similar to getting a brand new job, dropping a job, receiving a promotion, or creating a further income stream.

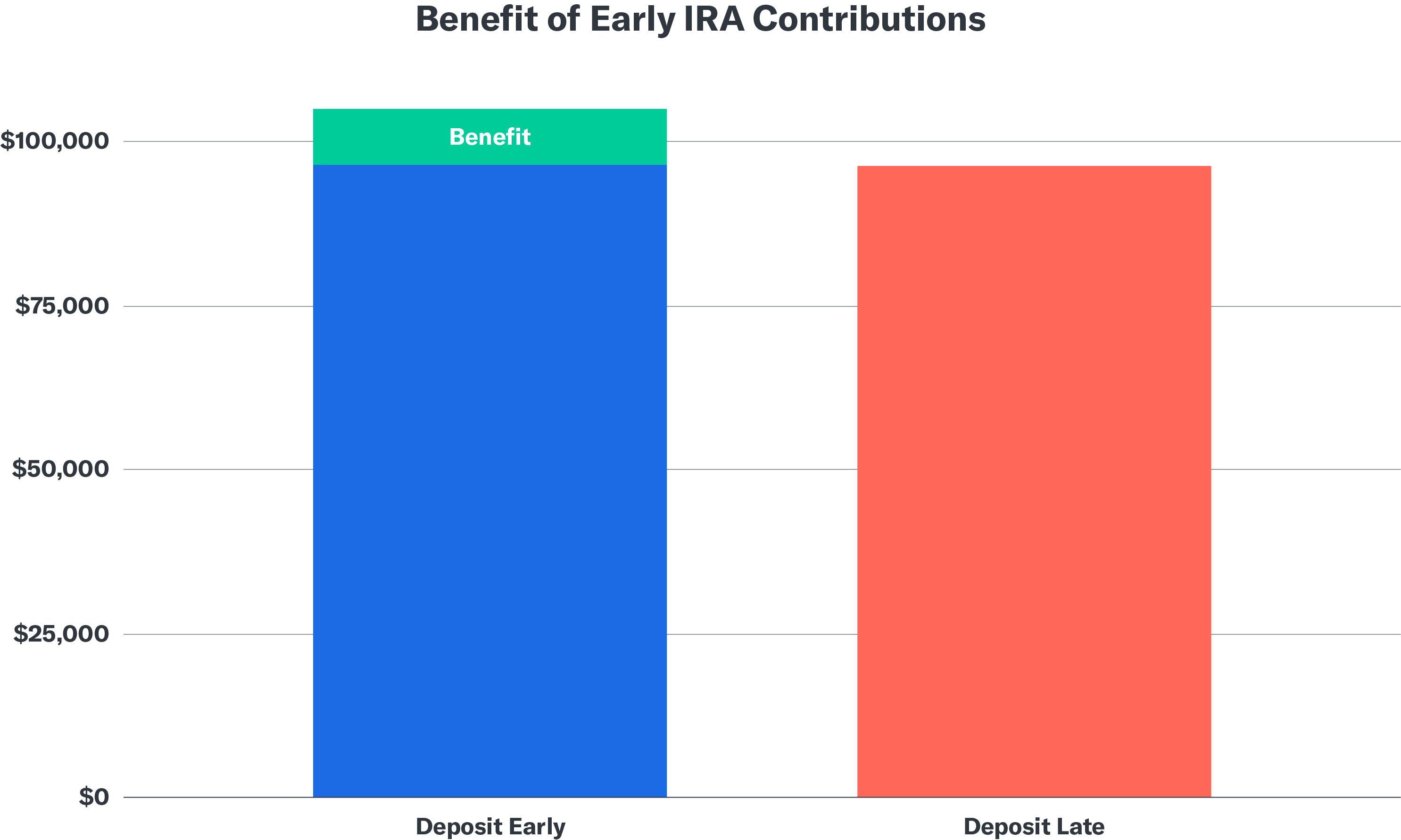

Timing IRA contributions: why earlier is best

No matter which kind of IRA you choose, it helps to know how the timing of your contributions impacts your funding returns. It’s your option to both make a most contribution early within the yr, contribute over time, or wait till the deadline. By timing your contribution to be as early as doable, you may maximize your time out there, which may allow you to achieve extra returns over time.

Take into account the distinction between making a most contribution on January 1 and making it on December 1 annually. Then suppose, hypothetically, that your annual progress price is 10%. Right here’s what the distinction may appear to be between an IRA with early contributions and an IRA with late contributions:

What’s an IRA recharacterization?

You would possibly contribute to an IRA earlier than you’ve gotten began submitting your taxes and should not know precisely what your Modified Adjusted Gross Earnings will likely be for that yr. Due to this fact, it’s possible you’ll not know whether or not you’ll be eligible to contribute to a Roth IRA, or if it is possible for you to to deduct your contributions to a Conventional IRA.

In some instances, the IRS lets you reclassify your IRA contributions. A recharacterization adjustments your contributions (plus the features or minus the losses attributed to them) from a Conventional IRA to a Roth IRA, or, from a Roth IRA to a Conventional IRA. It’s commonest to recharacterize a Roth IRA to a Conventional IRA.

Usually, there are not any taxes related to a recharacterization if the quantity you recharacterize consists of features or excludes {dollars} misplaced.

Listed here are three situations the place a recharacterization could also be best for you:

- In the event you made a Roth contribution through the yr however found later that your earnings was excessive sufficient to cut back the quantity you have been allowed to contribute—or prohibit you from contributing in any respect.

- In the event you contributed to a Conventional IRA since you thought your earnings can be above the allowed limits for a Roth IRA contribution, however your earnings ended up decrease than you’d anticipated.

- In the event you contributed to a Roth IRA, however whereas making ready your tax return, you understand that you simply’d profit extra from the instant tax deduction a Conventional IRA contribution would probably present.

Moreover, we’ve got listed just a few strategies that can be utilized to appropriate an over-contribution to an IRA on this FAQ useful resource.

You can’t recharacterize an quantity that’s greater than your allowable most annual contribution. You have got till annually’s tax submitting deadline to recharacterize—until you file for an extension otherwise you file an amended tax return.

What’s a Roth conversion?

A Roth conversion is a one-way road. It’s a probably taxable occasion the place funds are transferred from a Conventional IRA to a Roth IRA. There isn’t a such factor as a Roth to Conventional conversion. It’s totally different from a recharacterization as a result of you aren’t altering the kind of IRA that you simply contributed to for that individual yr. There isn’t a cap on the quantity that’s eligible to be transformed, so the sky’s the restrict for people who select to transform. We go into Roth conversions in additional element in our Assist Middle.

{kind=link}