Completely satisfied New Yr to all our common readers!

We’re kicking off 2025 with a countdown of what we expect had been the ten most fascinating charts from our blogs in 2024.

As you’ll see, we coated loads of totally different subjects – from introductions to choices and quick promoting to latency to creating markets higher for issuers and traders.

We begin our countdown at quantity 10:

10. Our first interns’ information to choices

In 2024, we added to our suite of normal summer season interns’ guides. Along with introductions to market construction, how buying and selling works and ETFs, we added a information to choices markets.

This included loads of info, akin to how choice payoffs work, the place the liquidity in U.S. choices markets is, and when and the way every choice expires (Together with a helpful desk exhibiting what choices expire within the open vs. the shut, and which have bodily supply).

However my favourite chart from the weblog regarded on the “moneyness” of choices being traded. Because the chart exhibits, the vast majority of choices being traded when they’re “out of the cash.” That considerably reduces the premium prices (because the chance of train is decrease) and the quantity of hedging a market maker would want to do (because the delta is decrease). It additionally implies that including up “choices notional worth traded” supplies a meaningless comparability to liquidity in underlying shares because the exposures and hedging are each properly beneath 1-to-1.

Chart 10: Most choices are commerce when they’re out of the cash

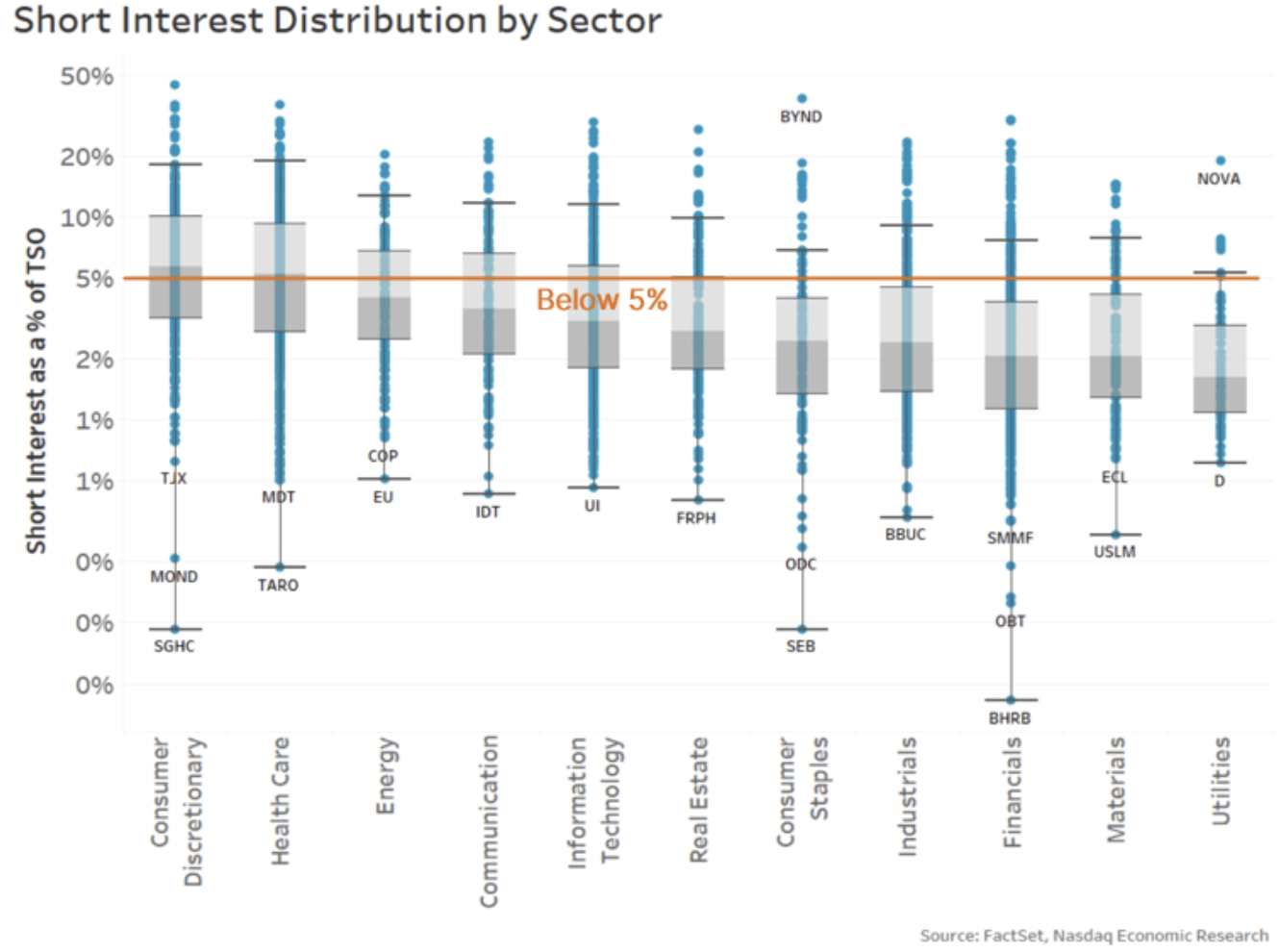

9. Brief curiosity isn’t as scary because it appears

It is truthful to say that traders and firms each don’t prefer it when their inventory costs fall. Nonetheless, it’s often fallacious to focus blame on quick sellers.

As we detailed in a weblog in 2024, there’s knowledge accessible to assist us perceive some points of quick promoting.

First, we noticed that regardless of a really excessive proportion of trades having a “quick promote” flag on them, the precise ranges of quick curiosity (or holdings) available in the market are usually a lot decrease and steady. Because the chart beneath exhibits, most shares have 5% or much less of their shares excellent held quick. That confirms that the majority quick promoting is completed by “bona-fide market makers” who’re required to promote and purchase all day (to qualify as a market maker) and never including to directional positions.

We additionally cited guidelines that require inventory to be borrowed earlier than settlement. That’s so consumers can obtain the inventory they purchased from a “quick” vendor – as with out that, the commerce would “fail.” And knowledge exhibits that failing trades are comparatively uncommon, and most fails are for exceptionally small (most definitely retail) trades.

Chart 9: Most shares have beneath 5% of their shares excellent shorted

It’s additionally essential to notice that analysis constantly exhibits that quick promoting makes markets extra environment friendly. It permits for hedging and cross-market arbitrage to happen, which helps hold Futures and ETF costs appropriate and inventory spreads tight.

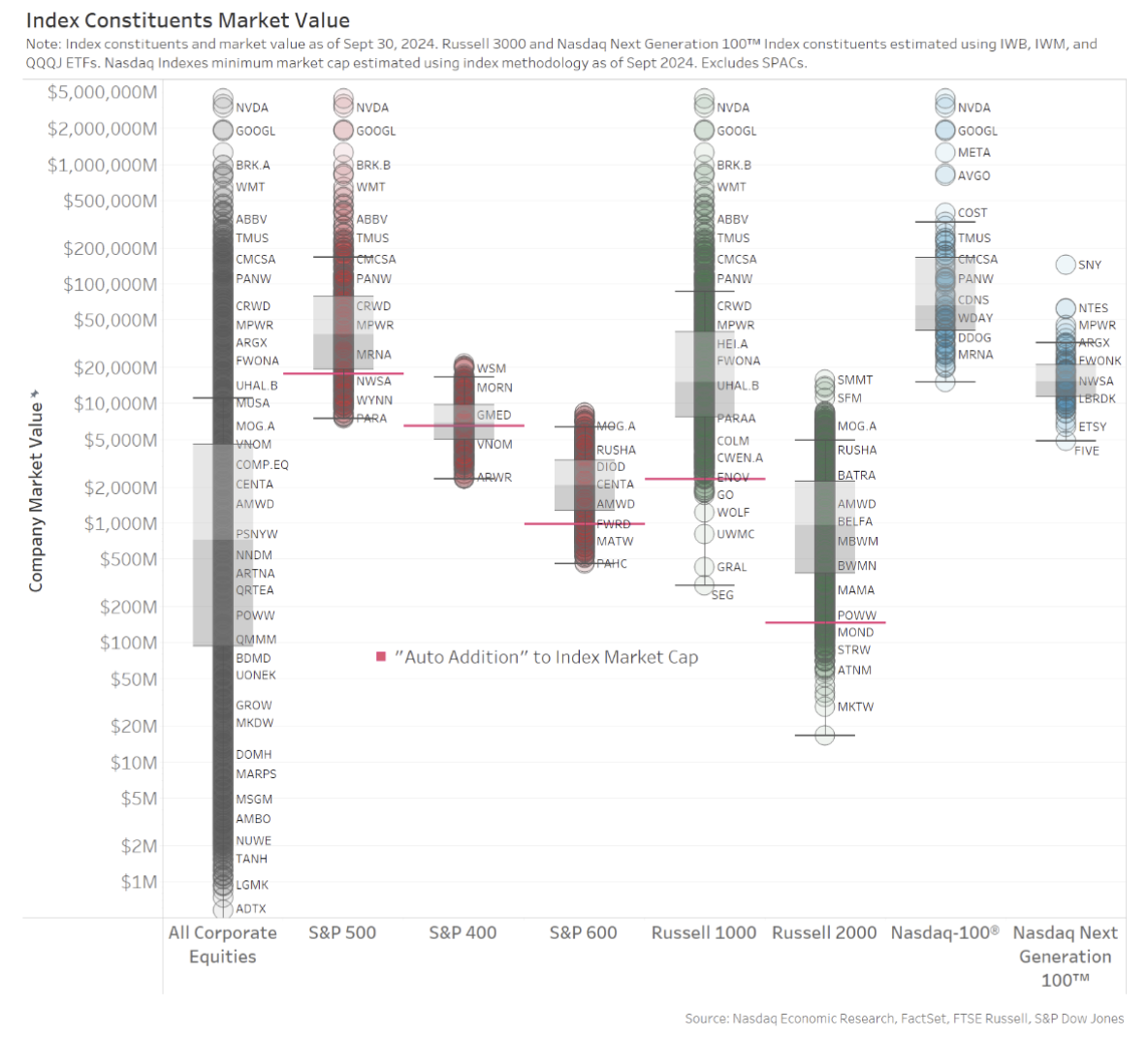

8. What defines a small-cap inventory will depend on the index supplier

Folks continuously discuss large-, mid- and small-cap shares – as whether it is clear what firms are included in every group.

Nonetheless, our favourite chart from that research exhibits that it may rely rather a lot on which index supplier you’re utilizing. In truth, the chart beneath exhibits that some small-cap shares are bigger than the smallest large-cap shares. Though to be truthful, that’s a results of value adjustments throughout the 12 months in addition to a acutely aware choice to scale back index turnover and buying and selling value for anybody operating an index fund.

Chart 8: Shares included in numerous market cap indexes by index supplier

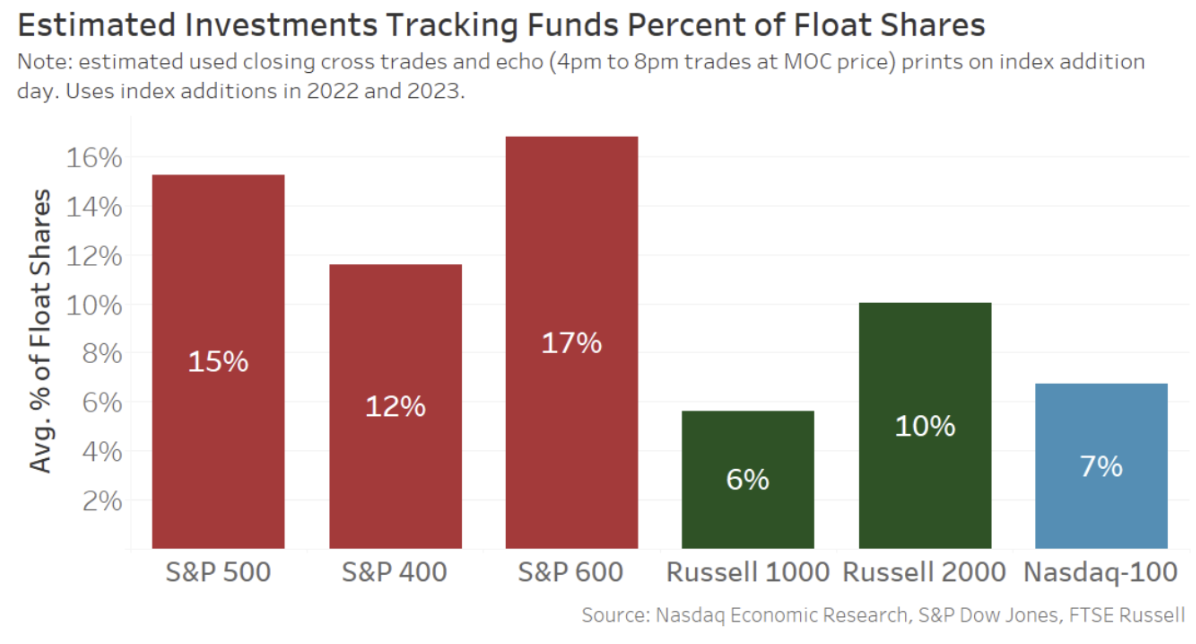

7. Taking a look at index trades to estimate index monitoring

Index funds and ETFs are getting extra and extra standard.

In one other research, we checked out how a lot of an organization’s accessible shares commerce within the shut on an index addition date.

The outcomes had been revealing, exhibiting that the market can present an enormous quantity of liquidity immediately because the market closes with the intention to fulfill indexer demand. That’s much more spectacular given latest analysis exhibits the value of that liquidity has been falling whilst index funds continued to develop.

Chart 7: The MOC is ready to take up big quantities of liquidity on index rebalance dates

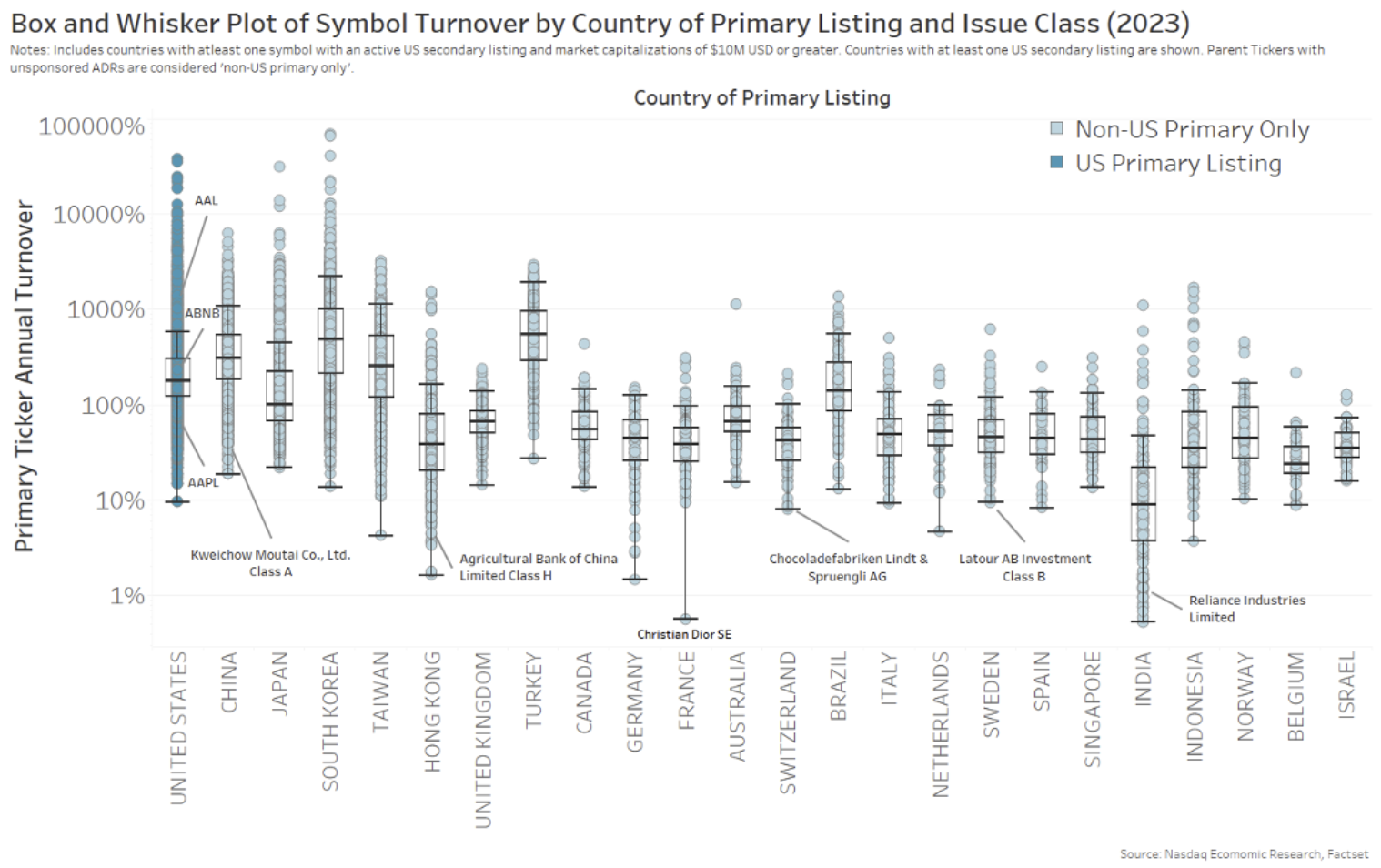

6. Is the U.S. actually probably the most liquid market on the planet?

Folks continuously boast about how the U.S. is the most cost effective, most liquid fairness market to commerce on the planet.

Nonetheless, with roughly 6,000 firms listed within the U.S. versus lower than 900 firms listed in France, is it even truthful to check buying and selling in Apple to Whole?

It is fairer if we compute the “market-cap turnover” of every firm, which is measured because the instances the overall accessible shares commerce annually. That accounts for various share costs and market caps around the globe.

The consequence (as we present within the chart beneath) was revealing. U.S. liquidity was good, however not the best. Notably, liquidity in plenty of Asian nations – with typically robust retail markets – was, on common, even higher. Though, as one other chart in that research confirmed, Asia’s bigger developed markets dragged the common for the entire area down beneath that of the U.S.

Chart 6: Annual market-cap turnover for every inventory (by nation)

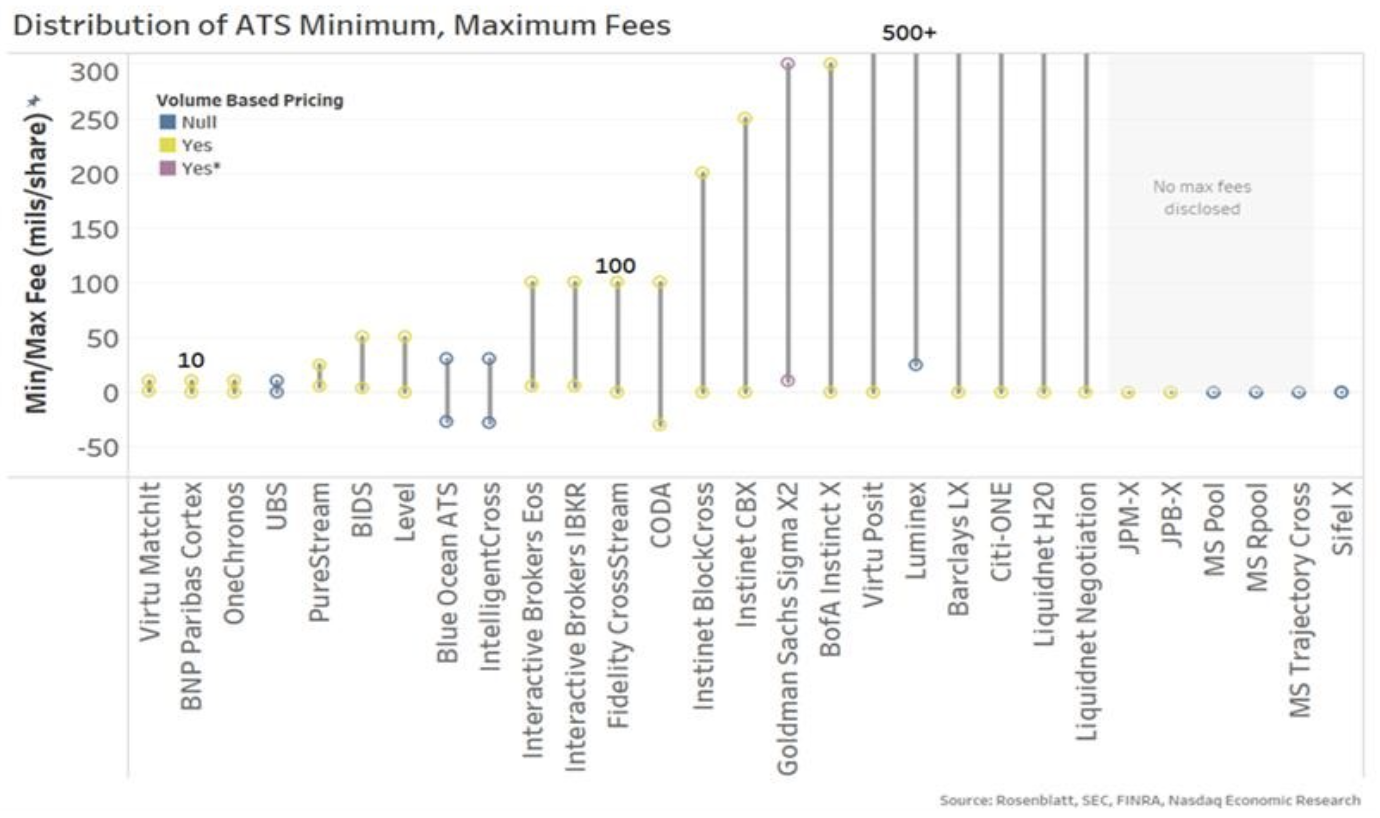

5. Exchanges charges work very in a different way to ATS’s

The U.S. Securities and Trade Fee (SEC) was extraordinarily busy in 2024, finalizing a large number of recent guidelines. A couple of focused exchanges and their payment buildings, together with lowering entry charges and eliminating quantity reductions for lcustomers who commerce and quote rather a lot.

These guidelines solely affected how change charges work, which was ironic, provided that 2024 was additionally the 12 months that off-exchange buying and selling handed the 50% mark (greater than as soon as). That’s particularly essential because it’s a stage thought of a tipping level important to market high quality and having an NBBO that’s significant to the market and really protects traders.

In brief, by specializing in change charges, the SEC missed the more and more aggressive economics of the “different half” of the market.

We have now stated earlier than that equal isn’t truthful. That’s one thing that appears undeniably clear whenever you take a look at charges charged for the SIP (which embrace quantity reductions) and the way the SEC recoups its annual finances (which varies over time).

The economics of the “different half” of the market may be very totally different. Relatively than being truthful entry and equal (just like the SEC desires for exchanges), it’s bilateral and bundled, with buyer high quality tiers and segmentation that provides to unfold seize (permitting charges to be larger). In truth, because the chart beneath from this weblog highlighted, ATSs cost a variety of charges – from “free” to a lot larger than the present change payment cap.

Both manner, “ten” is clearly not the norm, nor might or not it’s stated that different charges within the market are “equal”.

Chart 5: Kind ATS-N exhibits simply how difficult market pricing is throughout (even off-exchange) venues

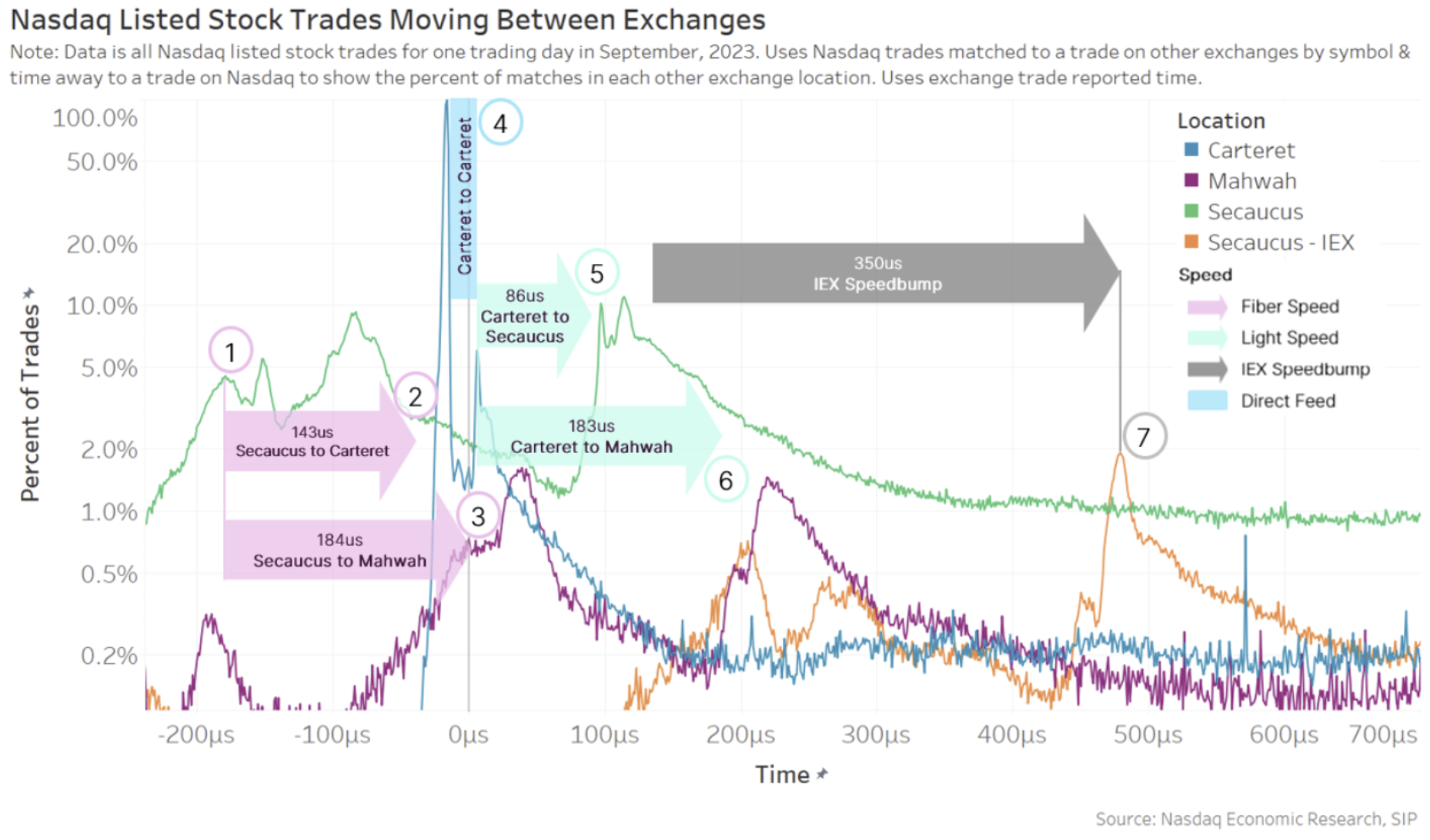

4. One millisecond is just de minimis to a human

Years in the past, the SEC created a brand new “de minimis” rule designed solely to approve IEX’s velocity bump market (the identical 12 months they denied Cboe their very own velocity bump proposal, which was solely fractionally slower). The SEC has since leaned on that rule to approve IEX’s D-limit (fade-able however protected) lit quotes. Satirically, the U.S. regulator declined to make use of it for figuring out an acceptable stage of latency for the SIP.

All of that historical past is related to a research of buying and selling latency we did in 2024.

What we mentioned in that weblog was how, even on the velocity of sunshine, it takes time for a commerce to journey across the U.S. market for fills, which occur in real-time, fractions of a second aside, inflicting reverberations throughout the market.

In truth, what our favourite chart from that weblog confirmed, utilizing microsecond timestamps (one-thousandth of a millisecond) is that we are able to see loads of trades within the U.S. market provoke from Secaucus, the place most dealer algorithms are positioned. Initially, the orders from these algorithms journey at fiber velocity across the U.S. market (pink arrows), then, as fills are seen at every venue, a response appears to happen at microwave speeds (inexperienced arrows) earlier than lastly passing via the IEX velocity bump and buying and selling there final, if any of their quotes haven’t, by then, been repriced.

Even with the IEX velocity bump delaying trades occurring on their venue, from begin to end, this all occurs in lower than 1 millisecond.

Chart 4: Trades journey across the U.S. market and trigger reactions that final lower than one millisecond

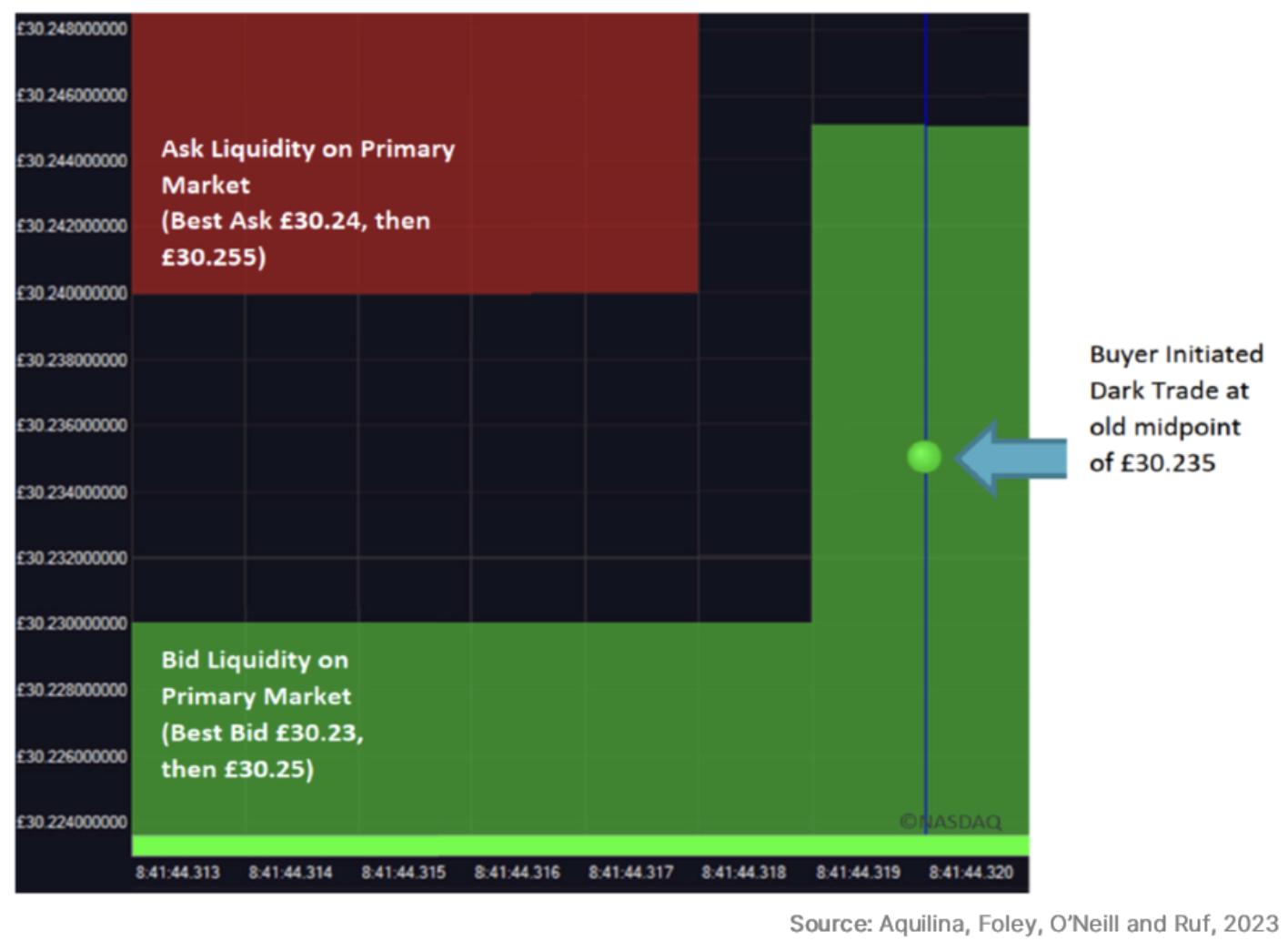

3. Latency arbitrage detected in London darkish swimming pools

What we discuss in Chart 4 above is what leads folks to speak about latency arbitrage. A brand new tutorial research confirmed how this may work in follow in darkish swimming pools in the UK.

Darkish swimming pools, by design, peg orders to the quotes set by exchanges. The chart from that weblog that the majority clearly confirmed what they discovered is beneath. It exhibits:

- The bid on change growing (inexperienced colour).

- Earlier than a fill happens in a darkish pool on the “outdated midpoint.”

That is doable as a result of “quick” arbitrageurs can ship a commerce on microwave, whereas quotes journey on optic fiber (which has a slower velocity of sunshine however is extra dependable).

The research discovered that “a considerable quantity of stale buying and selling happens [in dark pools].” In addition they discovered that arbitrageurs had been on the profitable facet of the commerce greater than 96% of the time – shopping for on the stale midpoint whereas promoting on the major markets at a more recent, larger value.

Chart 3: Darkish fills occurring at outdated midpoints because of distance-created latency

It has since been replicated throughout Europe, with analysis from Euronext, SIX Swiss and Deutsche Börse discovering comparable outcomes.

This research has essential implications for the consolidated tape debates occurring in Europe and elsewhere.

As we’ve stated earlier than, all costs are delayed, and a consolidated tape will all the time be (even) slower. That’s why even our rivals say a consolidated tape ought to by no means be used for buying and selling.

Stated one other manner, a consolidated tape can by no means be pre-trade (it’s simply physics). Nonetheless, it could possibly be used to quantify how a lot buying and selling is going on at these stale quotes.

This has market construction implications, too. The fragmentation reduces the fill chance to darkish pool clients (even when a purchaser crossed the lit market unfold) but additionally makes unfold seize more durable on the first market more durable (as unfold crossers are largely extra aggressive trades). The result’s worse economics for value setters and finally wider spreads and fewer depth.

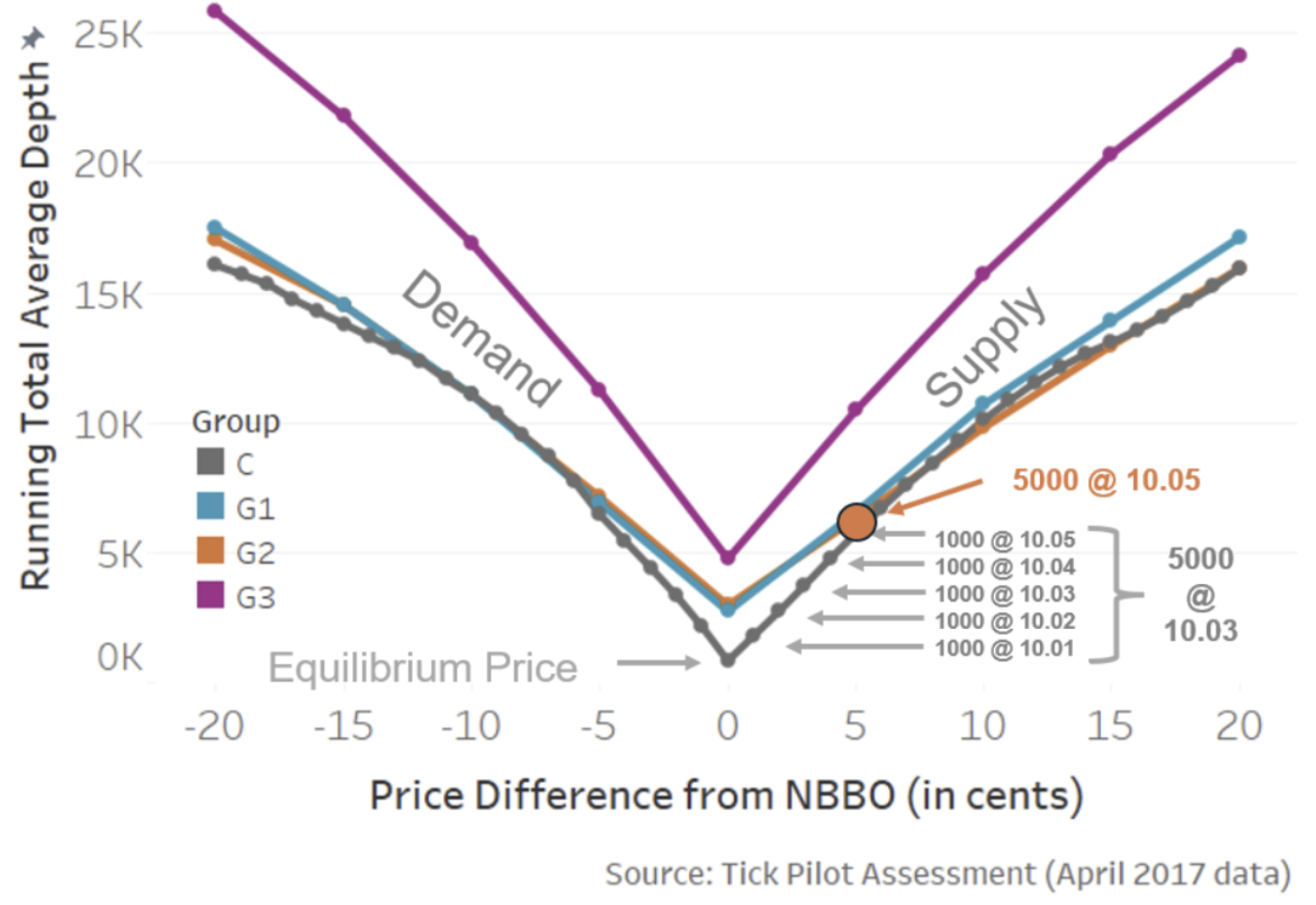

2. Depth and spreads react to fundamental economics of provide and demand

Tick sizes have been studied in depth by us and teachers. The findings are all fairly constant, exhibiting that the economics of spreads and depth are pushed by easy provide and demand.

Within the weblog the place we summarized these findings, probably the most related chart is the one beneath. It exhibits that:

- Provide and demand curves for shares are usually fairly linear.

- Lowering the tick (for tick-constrained shares) helps to cut back not solely the unfold but additionally the depth. For traders, spreads and depth are a trade-off.

Primarily based on all of the research, the one consequence that was capable of enhance each spreads and depth of the NBBO was the trade-at group within the Tick Pilot research (proven as G3 beneath). Apparently, that’s what occurs when the worth setter will get to seize their very own unfold – quite than BBO getting used to commerce elsewhere like we see in chart 3 above.

Chart 2: Analysis exhibits bettering spreads virtually all the time worsens depth; it’s a trade-off with out trade-at

1. Nasdaq has higher auctions for issuers

Throughout 2024, we noticed the five hundredth firm swap from NYSE to Nasdaq.

Clearly, all of us commerce in an NMS world (Nationwide Market System) with UTP (unlisted buying and selling privileges) which means shares can commerce anyplace – no matter the place they’re listed.

However after we take a look at the info, we see that Nasdaq market high quality is nonetheless higher for firms.

Our favourite chart from that weblog regarded on the open and shutting auctions. It exhibits that totally different public sale guidelines can scale back a inventory’s volatility. That’s essential as a result of analysis means that it may scale back an organization’s value of capital, which ought to result in further investments and returns for traders. This, in flip, is sweet for the U.S. financial system.

Chart 1: Switches have decrease public sale volatility on Nasdaq

We hope everybody had a cheerful and wholesome vacation season. We’re wanting ahead to bringing extra new and fascinating insights all through 2025.

Completely satisfied New Yr to all our common readers!

We’re kicking off 2025 with a countdown of what we expect had been the ten most fascinating charts from our blogs in 2024.

As you’ll see, we coated loads of totally different subjects – from introductions to choices and quick promoting to latency to creating markets higher for issuers and traders.

We begin our countdown at quantity 10:

10. Our first interns’ information to choices

In 2024, we added to our suite of normal summer season interns’ guides. Along with introductions to market construction, how buying and selling works and ETFs, we added a information to choices markets.

This included loads of info, akin to how choice payoffs work, the place the liquidity in U.S. choices markets is, and when and the way every choice expires (Together with a helpful desk exhibiting what choices expire within the open vs. the shut, and which have bodily supply).

However my favourite chart from the weblog regarded on the “moneyness” of choices being traded. Because the chart exhibits, the vast majority of choices being traded when they’re “out of the cash.” That considerably reduces the premium prices (because the chance of train is decrease) and the quantity of hedging a market maker would want to do (because the delta is decrease). It additionally implies that including up “choices notional worth traded” supplies a meaningless comparability to liquidity in underlying shares because the exposures and hedging are each properly beneath 1-to-1.

Chart 10: Most choices are commerce when they’re out of the cash

9. Brief curiosity isn’t as scary because it appears

It is truthful to say that traders and firms each don’t prefer it when their inventory costs fall. Nonetheless, it’s often fallacious to focus blame on quick sellers.

As we detailed in a weblog in 2024, there’s knowledge accessible to assist us perceive some points of quick promoting.

First, we noticed that regardless of a really excessive proportion of trades having a “quick promote” flag on them, the precise ranges of quick curiosity (or holdings) available in the market are usually a lot decrease and steady. Because the chart beneath exhibits, most shares have 5% or much less of their shares excellent held quick. That confirms that the majority quick promoting is completed by “bona-fide market makers” who’re required to promote and purchase all day (to qualify as a market maker) and never including to directional positions.

We additionally cited guidelines that require inventory to be borrowed earlier than settlement. That’s so consumers can obtain the inventory they purchased from a “quick” vendor – as with out that, the commerce would “fail.” And knowledge exhibits that failing trades are comparatively uncommon, and most fails are for exceptionally small (most definitely retail) trades.

Chart 9: Most shares have beneath 5% of their shares excellent shorted

It’s additionally essential to notice that analysis constantly exhibits that quick promoting makes markets extra environment friendly. It permits for hedging and cross-market arbitrage to happen, which helps hold Futures and ETF costs appropriate and inventory spreads tight.

8. What defines a small-cap inventory will depend on the index supplier

Folks continuously discuss large-, mid- and small-cap shares – as whether it is clear what firms are included in every group.

Nonetheless, our favourite chart from that research exhibits that it may rely rather a lot on which index supplier you’re utilizing. In truth, the chart beneath exhibits that some small-cap shares are bigger than the smallest large-cap shares. Though to be truthful, that’s a results of value adjustments throughout the 12 months in addition to a acutely aware choice to scale back index turnover and buying and selling value for anybody operating an index fund.

Chart 8: Shares included in numerous market cap indexes by index supplier

7. Taking a look at index trades to estimate index monitoring

Index funds and ETFs are getting extra and extra standard.

In one other research, we checked out how a lot of an organization’s accessible shares commerce within the shut on an index addition date.

The outcomes had been revealing, exhibiting that the market can present an enormous quantity of liquidity immediately because the market closes with the intention to fulfill indexer demand. That’s much more spectacular given latest analysis exhibits the value of that liquidity has been falling whilst index funds continued to develop.

Chart 7: The MOC is ready to take up big quantities of liquidity on index rebalance dates

6. Is the U.S. actually probably the most liquid market on the planet?

Folks continuously boast about how the U.S. is the most cost effective, most liquid fairness market to commerce on the planet.

Nonetheless, with roughly 6,000 firms listed within the U.S. versus lower than 900 firms listed in France, is it even truthful to check buying and selling in Apple to Whole?

It is fairer if we compute the “market-cap turnover” of every firm, which is measured because the instances the overall accessible shares commerce annually. That accounts for various share costs and market caps around the globe.

The consequence (as we present within the chart beneath) was revealing. U.S. liquidity was good, however not the best. Notably, liquidity in plenty of Asian nations – with typically robust retail markets – was, on common, even higher. Though, as one other chart in that research confirmed, Asia’s bigger developed markets dragged the common for the entire area down beneath that of the U.S.

Chart 6: Annual market-cap turnover for every inventory (by nation)

5. Exchanges charges work very in a different way to ATS’s

The U.S. Securities and Trade Fee (SEC) was extraordinarily busy in 2024, finalizing a large number of recent guidelines. A couple of focused exchanges and their payment buildings, together with lowering entry charges and eliminating quantity reductions for lcustomers who commerce and quote rather a lot.

These guidelines solely affected how change charges work, which was ironic, provided that 2024 was additionally the 12 months that off-exchange buying and selling handed the 50% mark (greater than as soon as). That’s particularly essential because it’s a stage thought of a tipping level important to market high quality and having an NBBO that’s significant to the market and really protects traders.

In brief, by specializing in change charges, the SEC missed the more and more aggressive economics of the “different half” of the market.

We have now stated earlier than that equal isn’t truthful. That’s one thing that appears undeniably clear whenever you take a look at charges charged for the SIP (which embrace quantity reductions) and the way the SEC recoups its annual finances (which varies over time).

The economics of the “different half” of the market may be very totally different. Relatively than being truthful entry and equal (just like the SEC desires for exchanges), it’s bilateral and bundled, with buyer high quality tiers and segmentation that provides to unfold seize (permitting charges to be larger). In truth, because the chart beneath from this weblog highlighted, ATSs cost a variety of charges – from “free” to a lot larger than the present change payment cap.

Both manner, “ten” is clearly not the norm, nor might or not it’s stated that different charges within the market are “equal”.

Chart 5: Kind ATS-N exhibits simply how difficult market pricing is throughout (even off-exchange) venues

4. One millisecond is just de minimis to a human

Years in the past, the SEC created a brand new “de minimis” rule designed solely to approve IEX’s velocity bump market (the identical 12 months they denied Cboe their very own velocity bump proposal, which was solely fractionally slower). The SEC has since leaned on that rule to approve IEX’s D-limit (fade-able however protected) lit quotes. Satirically, the U.S. regulator declined to make use of it for figuring out an acceptable stage of latency for the SIP.

All of that historical past is related to a research of buying and selling latency we did in 2024.

What we mentioned in that weblog was how, even on the velocity of sunshine, it takes time for a commerce to journey across the U.S. market for fills, which occur in real-time, fractions of a second aside, inflicting reverberations throughout the market.

In truth, what our favourite chart from that weblog confirmed, utilizing microsecond timestamps (one-thousandth of a millisecond) is that we are able to see loads of trades within the U.S. market provoke from Secaucus, the place most dealer algorithms are positioned. Initially, the orders from these algorithms journey at fiber velocity across the U.S. market (pink arrows), then, as fills are seen at every venue, a response appears to happen at microwave speeds (inexperienced arrows) earlier than lastly passing via the IEX velocity bump and buying and selling there final, if any of their quotes haven’t, by then, been repriced.

Even with the IEX velocity bump delaying trades occurring on their venue, from begin to end, this all occurs in lower than 1 millisecond.

Chart 4: Trades journey across the U.S. market and trigger reactions that final lower than one millisecond

3. Latency arbitrage detected in London darkish swimming pools

What we discuss in Chart 4 above is what leads folks to speak about latency arbitrage. A brand new tutorial research confirmed how this may work in follow in darkish swimming pools in the UK.

Darkish swimming pools, by design, peg orders to the quotes set by exchanges. The chart from that weblog that the majority clearly confirmed what they discovered is beneath. It exhibits:

- The bid on change growing (inexperienced colour).

- Earlier than a fill happens in a darkish pool on the “outdated midpoint.”

That is doable as a result of “quick” arbitrageurs can ship a commerce on microwave, whereas quotes journey on optic fiber (which has a slower velocity of sunshine however is extra dependable).

The research discovered that “a considerable quantity of stale buying and selling happens [in dark pools].” In addition they discovered that arbitrageurs had been on the profitable facet of the commerce greater than 96% of the time – shopping for on the stale midpoint whereas promoting on the major markets at a more recent, larger value.

Chart 3: Darkish fills occurring at outdated midpoints because of distance-created latency

It has since been replicated throughout Europe, with analysis from Euronext, SIX Swiss and Deutsche Börse discovering comparable outcomes.

This research has essential implications for the consolidated tape debates occurring in Europe and elsewhere.

As we’ve stated earlier than, all costs are delayed, and a consolidated tape will all the time be (even) slower. That’s why even our rivals say a consolidated tape ought to by no means be used for buying and selling.

Stated one other manner, a consolidated tape can by no means be pre-trade (it’s simply physics). Nonetheless, it could possibly be used to quantify how a lot buying and selling is going on at these stale quotes.

This has market construction implications, too. The fragmentation reduces the fill chance to darkish pool clients (even when a purchaser crossed the lit market unfold) but additionally makes unfold seize more durable on the first market more durable (as unfold crossers are largely extra aggressive trades). The result’s worse economics for value setters and finally wider spreads and fewer depth.

2. Depth and spreads react to fundamental economics of provide and demand

Tick sizes have been studied in depth by us and teachers. The findings are all fairly constant, exhibiting that the economics of spreads and depth are pushed by easy provide and demand.

Within the weblog the place we summarized these findings, probably the most related chart is the one beneath. It exhibits that:

- Provide and demand curves for shares are usually fairly linear.

- Lowering the tick (for tick-constrained shares) helps to cut back not solely the unfold but additionally the depth. For traders, spreads and depth are a trade-off.

Primarily based on all of the research, the one consequence that was capable of enhance each spreads and depth of the NBBO was the trade-at group within the Tick Pilot research (proven as G3 beneath). Apparently, that’s what occurs when the worth setter will get to seize their very own unfold – quite than BBO getting used to commerce elsewhere like we see in chart 3 above.

Chart 2: Analysis exhibits bettering spreads virtually all the time worsens depth; it’s a trade-off with out trade-at

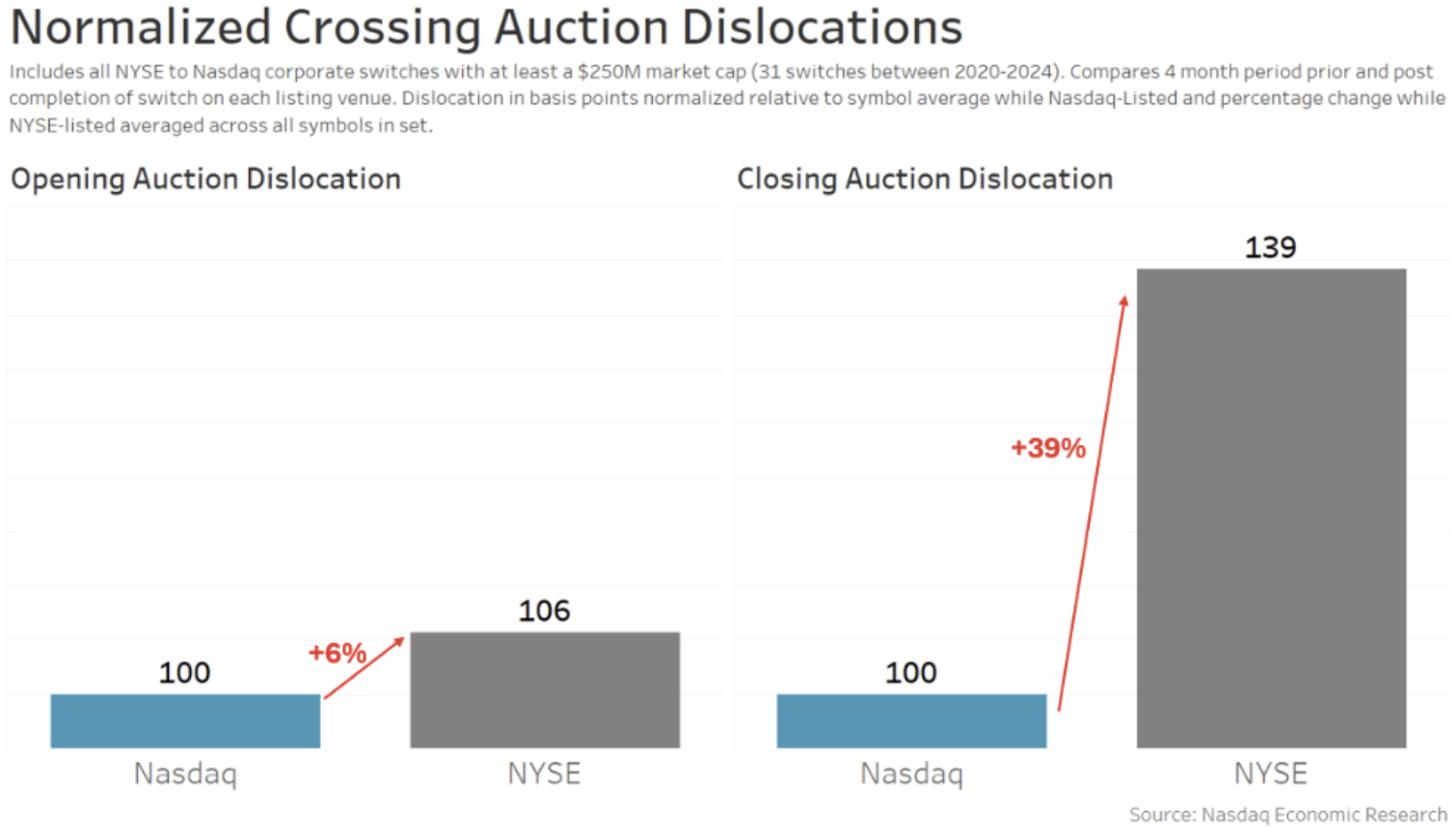

1. Nasdaq has higher auctions for issuers

Throughout 2024, we noticed the five hundredth firm swap from NYSE to Nasdaq.

Clearly, all of us commerce in an NMS world (Nationwide Market System) with UTP (unlisted buying and selling privileges) which means shares can commerce anyplace – no matter the place they’re listed.

However after we take a look at the info, we see that Nasdaq market high quality is nonetheless higher for firms.

Our favourite chart from that weblog regarded on the open and shutting auctions. It exhibits that totally different public sale guidelines can scale back a inventory’s volatility. That’s essential as a result of analysis means that it may scale back an organization’s value of capital, which ought to result in further investments and returns for traders. This, in flip, is sweet for the U.S. financial system.

Chart 1: Switches have decrease public sale volatility on Nasdaq

We hope everybody had a cheerful and wholesome vacation season. We’re wanting ahead to bringing extra new and fascinating insights all through 2025.

{kind=link}