MBW Reacts is a collection of analytical commentaries from Music Enterprise Worldwide written in response to main current leisure occasions or information tales. Solely MBW+ subscribers have limitless entry to those articles. The under article initially appeared inside Tim Ingham’s newest MBW+ Assessment electronic mail, issued solely to MBW+ subscribers.

So the elevator opens, and I discover myself face-to-face with Diana Ross.

True story. Throughout the Grammys earlier this month, mid-show, I took a elevate – as we are saying within the UK – down from the highest flooring of the Crypto Area to the bottom. And because the metallic doorways half, there, in all her chiffon finery, stands the Queen Of Motown.

I nearly managed to stutter, “Erm… hey, Ms. Ross.”

Had I discovered the phrases, I want I’d have beamed: “Ms. Ross – an honor! Can I say: (1) It’s a shame these fools by no means gave you a Grammy – aside from a paltry Lifetime Achievement sop – particularly throughout your imperial period, and (2) You being right here, handing out an award daring as brass, when this ceremony snubbed you so many instances, is punk rock AF. Thanks on behalf of Queen, Bob Marley, ABBA, Tupac, Oasis, Snoop, Weapons’N’Roses… and all the opposite cultural torchbearers this supposedly distinguished present has resolutely failed to acknowledge.”

Oh properly. “Erm… hey, Ms. Ross,” should do.

This interplay is of a theme.

The Grammys, just like the US report {industry} it represents, is typically so immersed in its personal acquired knowledge that it forgets to note seismic actions occurring proper underneath its nostril.

Sitting in Los Angeles, watching Kendrick Lamar and Beyoncé acquire golden gongs, the Grammys seems like the only real epicenter of the worldwide {industry}.

That is an America-first phantasm.

Instance: Because the 2025 version of ‘Music’s Largest Evening’ performed out, over in Tokyo, Common Music Group was busy negotiating the majority buy of Japanese label and administration firm A-Sketch.

In line with filings I’ve seen, UMG ultimately agreed to amass a 66% holding in A-Sketch – dwelling to J-pop stars Saucy Canine, Flumpool, and extra – for an preliminary quantity of 2.77 billion Yen, equal to round USD $18.2 million.

The vendor was Japan’s Amuse Inc; the opposite 34% of A-Sketch is owned by KDDI Company.

The A-Sketch deal adopted UMG’s 100% acqui

UMG has additionally been closely investing in different Asian territories – together with Indonesia, Vietnam, and Higher China (the place, in the previous couple of weeks, it signed a catalog-spanning deal with native legend, Liu Huan).

Wanting on the numbers, UMG’s aggressive growth in Asia is not any shock.

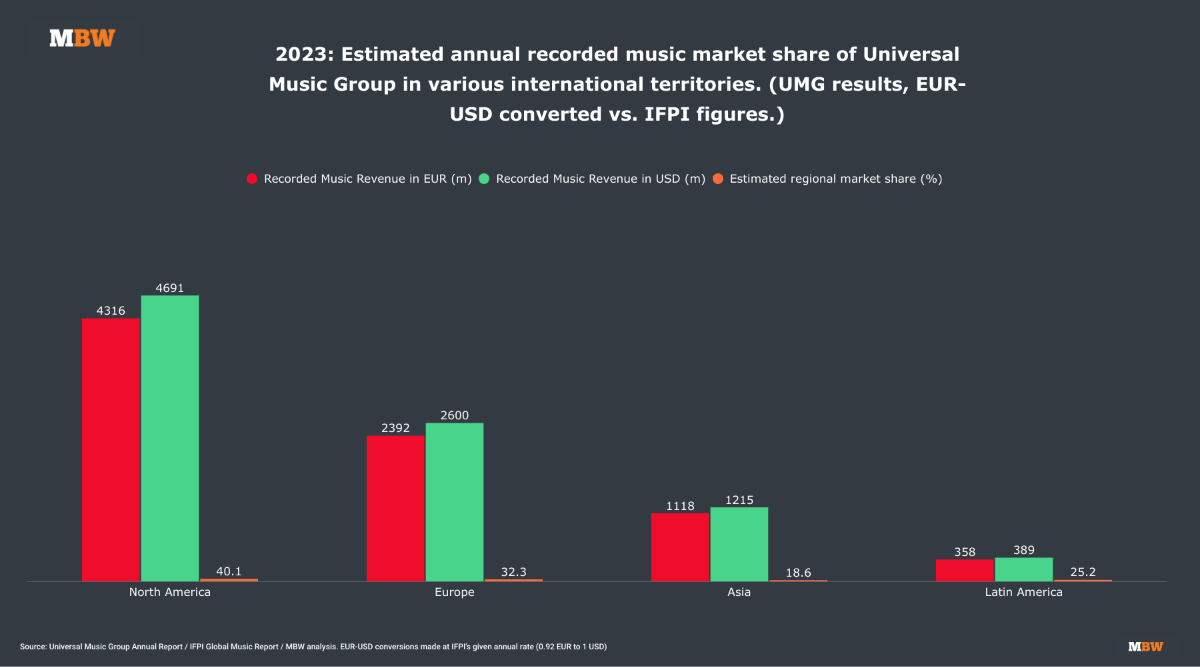

In line with its newest Annual Report, Common generated USD $4.7 billion in yearly recorded music (RM) revenues in North America in 2023 – representing some 51% of its world RM revenues.

Juxtaposed with IFPI {industry} knowledge, this means that UMG achieved a dominant market share of 40.1% in North America in 2023.

Over in Asia, although, issues look slightly completely different.

In APAC, UMG faces robust challenges from Sony (particularly in Japan), Imagine, and Warner, plus – most significantly – highly effective native rivals throughout territories like China, India, and South Korea.

In line with my calculations, Common generated roughly USD $1.2 billion in RM revenues in Asia in 2023 – implying an annual market share within the area (vs. IFPI’s figures) of 18.6%.

With offers like A-Sketch and RS Group – plus a flurry of current partnerships in China – we’re witnessing UMG’s dedication to push that quantity into the twenty-percents.

In the meantime, a separate macro image is additional pushing Common (and its rivals) to wager massive in Asia.

As a result of Asia, primarily pushed by the speedy progress of China, is beginning to gnaw into North America’s world music market share.

Right here’s a stat that hasn’t acquired almost sufficient consideration on this enterprise so far. I’ll make it purple to treatment this!

Asia grew quicker than North America as a recorded music market in 2023 based on IFPI knowledge. Not simply when it comes to proportion progress (Asia was up 14.9% YoY; North America up 7.4% YoY), however when it comes to actual financial improve in commerce revenues.

I received’t give away the precise figures (you’ll have to buy the full model of IFPI’s World Music Report for these), however right here’s a ballpark model: The annual commerce income of Asia’s recorded music enterprise grew by round USD $40 million extra than North America’s in 2023.

Certainly, when Europe and Asia are mixed, they signify greater than 50% of world recorded music revenues at this time… considerably greater than North America’s 41%.

It might need been refreshing to listen to such an worldwide actuality acknowledged from the stage on ‘Music’s Largest Evening’.

To be clear, Common’s comparatively small present market share in Asia vs. its dominance in North America is a reasonably pure scenario inside a report {industry} that has seen the US – off the again of streaming’s explosion – outstrip each different worldwide territory for the previous decade.

However now, the sport has modified – and UMG is responding.

The stats talked about right here underline how essential UMG’s growth in Asia will likely be for its ambition to rule music rights in an more and more globalized {industry} within the decade forward.

(Related sidenote: I had a number of conversations in Grammy Week with individuals who volunteered to guess who would possibly in the end succeed Sir Lucian Grainge as UMG boss. For starters, I can’t see Grainge going anyplace quickly, particularly if he’s capable of hold a minimum of two of UMG’s key shareholders – Tencent, Vincent Bolloré, and Invoice Ackman – completely happy. Certainly, with ‘Streaming 2.0’ in his sails and {the handcuffs} taken off UMG’s capacity to purchase within the EU, I think about Grainge is relishing the chance forward of him. Nevertheless it’s nonetheless fascinating to me that, amongst the post-Grainge-era prognosticators I’ve spoken to, John Janick and Monte Lipman are probably the most repeated hypothetical candidates for the highest job. This is sensible: as heads of UMG’s ‘West Coast’ and ‘East Coast’ Stateside label teams, they’re every working main revenue facilities for the corporate. But, once more, such an remark dangers carrying the bouquet of US-centricity: I humbly remind the jury that Adam Granite, EVP, is main UMG’s growth efforts in Asia and different ‘high-potential markets’, and is usually doing so in tandem with JT Myers and Nat Pastor. Myers and Pastor are co-CEOs of internationally-focused artist/label providers division Virgin Music Group, arguably Common’s No.1 strategic world precedence at this time. Because the worldwide music enterprise continues to internationalize, the remit of all these named right here – US-focused and less-US-focused – will solely develop in affect.)

Common’s acquisition of A-Sketch wasn’t the one massive Asia-related information of the previous week.

B2B distributor FUGA introduced a collection of key new partnerships in APAC, together with offers with labels in Indonesia, India, and the Philippines.

Which, in fact, brings us to one other matter.

On this MAGA-era of lessened regulation, it appears extremely prone to me that UMG (by way of VMG) can have no situation clearing its USD $775 million acquisition of FUGA’s proprietor, Downtown.

For proof, have a look at the UK, the place Sony memorably confronted a turbulent journey from competitors watchdog the CMA when shopping for AWAL in 2021.

British Prime Minister Keir Starmer, absolutely emboldened by Donald Trump’s mandate – and looking for fast funding into the UK – is at the moment defanging the once-prickly CMA. Starmer’s authorities simply overtly (and bluntly) instructed the CMA to create a “extra aggressive enterprise atmosphere with much less burdensome regulation”.

One irony right here: I believe UMG agreed to amass CD Child as a part of its Downtown purchase (pre-Trump) within the data that it might divest it from the deal if pushed to dump one thing by regulators.

These regulators (post-Trump) might now look the opposite means, leaving UMG to determine how the DIY distributor finest matches inside its stack of choices.

To a Western music enterprise that has grown comfy limiting its peripheral imaginative and prescient to the confines of North America and Europe, Common’s present market share in these two territories can be an comprehensible trigger for concern within the face of large-scale acquisitive strikes.

But once you broaden your view to territories exterior this duo – most notably the world’s fastest-growing music market, Asia – a extra rounded image emerges.

Common Music Group’s world market share at this time is removed from monopolistic.

UMG faces powerful and sizable competitors in areas exterior North America and Europe, each from dominant native gamers (see: T-Collection in India, for one), plus world rivals equally ravenous for progress.

(On that subject… right here’s one thing we forgot to report this week: Sony Corp simply confirmed on an earnings name that its Rob Stringer-led music division just lately acquired a significant catalog in India from Eros. Eros itself confirmed in its 2023 annual report that it had bought its complete music belongings portfolio to a “world music main entity”. We’re all the time watching !)

Past world music developments, right here’s one other easy argument that Common might current to regulators RE: issues about its Downtown purchase.

In comparison with Large Tech – together with music-involved Large Tech – even the music {industry}’s largest beasts seem like ‘indie’ minnows.

Google/Alphabet confirmed earlier this month that, in FY 2024, it generated $350 BILLION in annual revenues. Meta generated $164.5 BILLION; Apple generated $391 BILLION; Amazon generated $638 BILLION.

Cumulatively, these 4 corporations (all of which negotiate with UMG over licenses) generated over $1.5 TRILLION (!) final 12 months. Which means they collectively generate extra in a week than all the world recorded music enterprise manages in a 12 months.

Such comparisons depart accusations of monopolistic power-wielding by UMG wanting like intra-industry navel-gazing.

UMG’s ‘wins’ in its new offers with Amazon and Spotify – ‘wins’ that can now be replicated throughout this {industry} – exhibit the upsides of the music rights enterprise leaning on the combating energy of its very personal ‘900lb gorilla’.

If stated massive simian is to essentially flex its muscle groups in future, Asia is the territory to look at.Music Enterprise Worldwide

{kind=link}