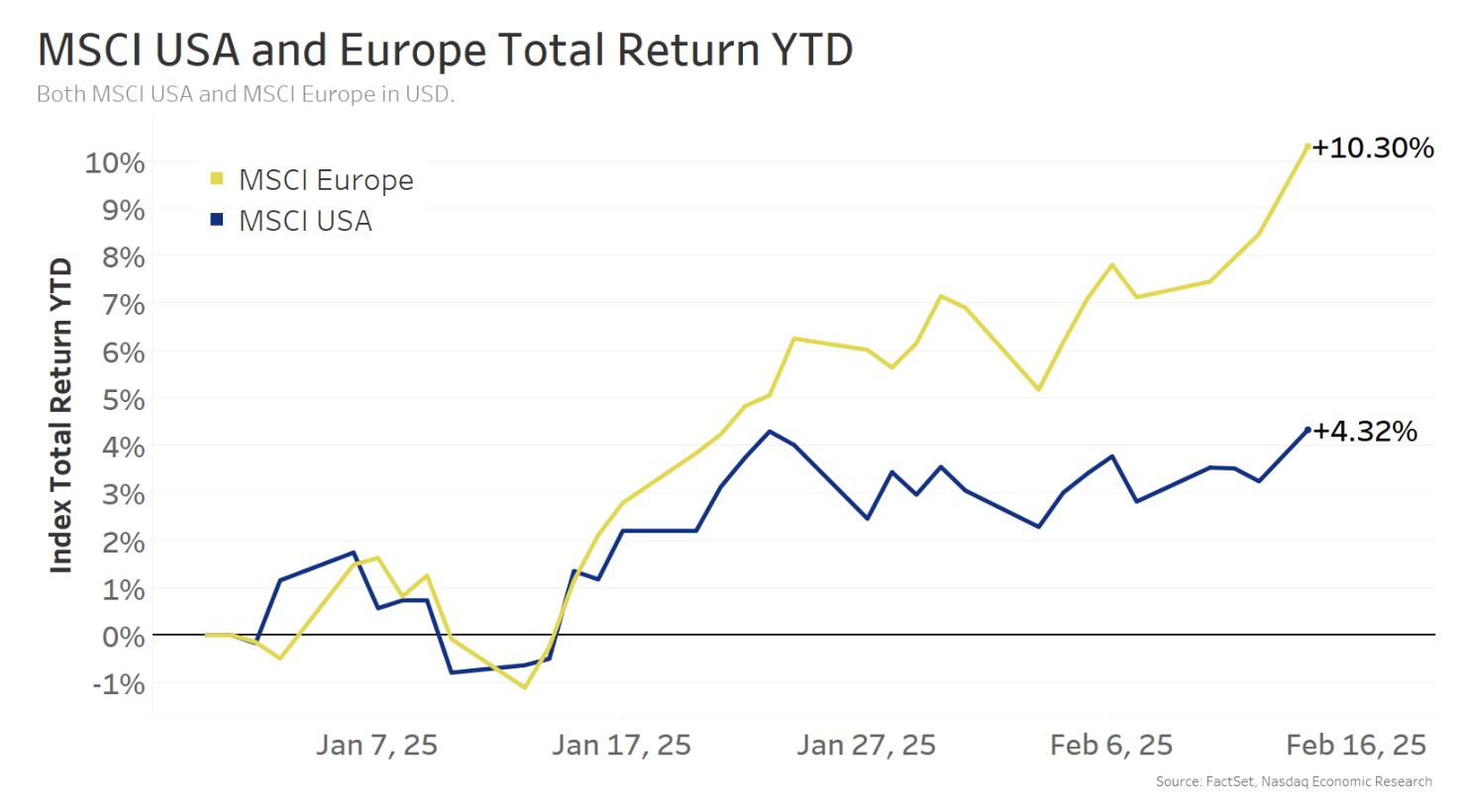

After 2 years of US Exceptionalism, Europe shares +10% YTD vs. +4% for the US

For the final couple years, the story for equities globally has been considered one of “US Exceptionalism,” the place US shares have considerably outperformed different markets, largely because of the US-based (and Nasdaq-listed) Magazine 7.

Over 2023 and 2024, US equities gained +59% – greater than double Europe’s +24% acquire (each measured by the MSCIindices of enormous and mid caps).

To start out 2025, although, the US hasn’t been so distinctive.

In reality, it’s Europe that’s doubling up the US, with the MSCI Europe up +10% (chart beneath, gold line), in comparison with +4% for the US (blue line).

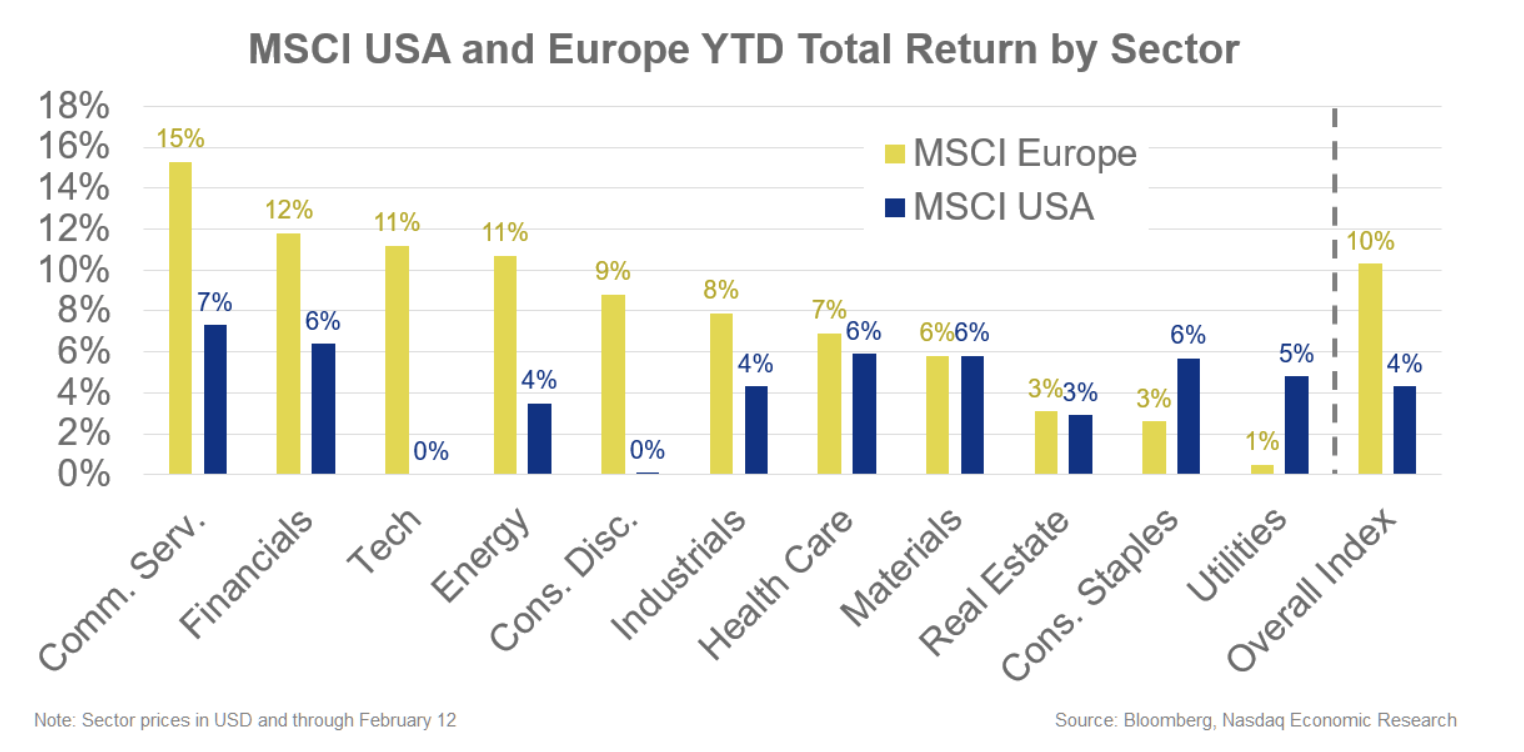

Europe’s lead is broad based mostly, beating the US throughout 7 of 11 sectors, tied in 2 extra

And it’s not only one factor driving it. If we take a look at returns this yr by sector (chart beneath), Europe (gold bars) is thrashing the US (blue bars) in 7 of 11 sectors, they usually’re basically tied in two extra (Supplies and Actual Property).

So Europe’s management is broad based mostly.

AI publicity, higher-for-longer charges, and “costly” valuations larger headwinds for US

There are just a few totally different causes the US has lagged Europe:

- US far more uncovered to AI. Tech is 40% of the MSCI USA in comparison with simply 10% for Europe. For the final 2 years, this favored the US, with AI optimism serving to the Magazine 7 acquire +156%. However the Magazine 7 is flat this yr, partly as a result of DeepSeek’s low price, excessive efficiency mannequin tempered that AI optimism (and the knowledge of Huge Tech’s deliberate $300bn spending on AI this yr). Europe, although, is tilted extra in direction of Financials, Well being Care, and Industrials.

- US dealing with higher-for-longer charges as Europe cuts. Markets are solely pricing 40bps in Fed cuts this yr, in comparison with 120bps from the European Central Financial institution (together with the 25bps reduce they already did). So the European financial system is anticipated to get extra of a lift from price cuts.

- Europe “low-cost” relative to US. The US’s Worth/Earnings valuation ratio is over 22 – near document highs throughout Covid and the Dotcom bubble – whereas Europe’s PE is simply over 14 – near its 20-year common and about two-thirds the US’s PE. So Europe shares are comparatively “low-cost” in comparison with the US. Plus, greater charges (#2) make it tougher to maintain excessive PEs since greater borrowing prices make future earnings tougher to comprehend.

- European earnings recession over. After seeing earnings fall -2% in 2024, the MSCI Europe is anticipated to see earnings rise +7% this yr. Although that trails the US’s projected +13% earnings acquire.

Nonetheless, exterior of the dimming of AI optimism, most of those components had been already in place to begin the yr.

So, it’s extra a narrative of Europe recovering (after gaining simply +2% final yr) than the US slowing down. In any case, the MSCI USA is slightly below its all-time excessive (set in January), and a +4.3% acquire in six weeks isn’t too unhealthy.

The data contained above is supplied for informational and academic functions solely, and nothing contained herein needs to be construed as funding recommendation, both on behalf of a selected safety or an general funding technique. Neither Nasdaq, Inc. nor any of its associates makes any advice to purchase or promote any safety or any illustration in regards to the monetary situation of any firm. Statements concerning Nasdaq-listed firms or Nasdaq proprietary indexes should not ensures of future efficiency. Precise outcomes could differ materially from these expressed or implied. Previous efficiency just isn’t indicative of future outcomes. Traders ought to undertake their very own due diligence and thoroughly consider firms earlier than investing. ADVICE FROM A SECURITIES PROFESSIONAL IS STRONGLY ADVISED. © 2024. Nasdaq, Inc. All Rights Reserved.

After 2 years of US Exceptionalism, Europe shares +10% YTD vs. +4% for the US

For the final couple years, the story for equities globally has been considered one of “US Exceptionalism,” the place US shares have considerably outperformed different markets, largely because of the US-based (and Nasdaq-listed) Magazine 7.

Over 2023 and 2024, US equities gained +59% – greater than double Europe’s +24% acquire (each measured by the MSCIindices of enormous and mid caps).

To start out 2025, although, the US hasn’t been so distinctive.

In reality, it’s Europe that’s doubling up the US, with the MSCI Europe up +10% (chart beneath, gold line), in comparison with +4% for the US (blue line).

Europe’s lead is broad based mostly, beating the US throughout 7 of 11 sectors, tied in 2 extra

And it’s not only one factor driving it. If we take a look at returns this yr by sector (chart beneath), Europe (gold bars) is thrashing the US (blue bars) in 7 of 11 sectors, they usually’re basically tied in two extra (Supplies and Actual Property).

So Europe’s management is broad based mostly.

AI publicity, higher-for-longer charges, and “costly” valuations larger headwinds for US

There are just a few totally different causes the US has lagged Europe:

- US far more uncovered to AI. Tech is 40% of the MSCI USA in comparison with simply 10% for Europe. For the final 2 years, this favored the US, with AI optimism serving to the Magazine 7 acquire +156%. However the Magazine 7 is flat this yr, partly as a result of DeepSeek’s low price, excessive efficiency mannequin tempered that AI optimism (and the knowledge of Huge Tech’s deliberate $300bn spending on AI this yr). Europe, although, is tilted extra in direction of Financials, Well being Care, and Industrials.

- US dealing with higher-for-longer charges as Europe cuts. Markets are solely pricing 40bps in Fed cuts this yr, in comparison with 120bps from the European Central Financial institution (together with the 25bps reduce they already did). So the European financial system is anticipated to get extra of a lift from price cuts.

- Europe “low-cost” relative to US. The US’s Worth/Earnings valuation ratio is over 22 – near document highs throughout Covid and the Dotcom bubble – whereas Europe’s PE is simply over 14 – near its 20-year common and about two-thirds the US’s PE. So Europe shares are comparatively “low-cost” in comparison with the US. Plus, greater charges (#2) make it tougher to maintain excessive PEs since greater borrowing prices make future earnings tougher to comprehend.

- European earnings recession over. After seeing earnings fall -2% in 2024, the MSCI Europe is anticipated to see earnings rise +7% this yr. Although that trails the US’s projected +13% earnings acquire.

Nonetheless, exterior of the dimming of AI optimism, most of those components had been already in place to begin the yr.

So, it’s extra a narrative of Europe recovering (after gaining simply +2% final yr) than the US slowing down. In any case, the MSCI USA is slightly below its all-time excessive (set in January), and a +4.3% acquire in six weeks isn’t too unhealthy.

The data contained above is supplied for informational and academic functions solely, and nothing contained herein needs to be construed as funding recommendation, both on behalf of a selected safety or an general funding technique. Neither Nasdaq, Inc. nor any of its associates makes any advice to purchase or promote any safety or any illustration in regards to the monetary situation of any firm. Statements concerning Nasdaq-listed firms or Nasdaq proprietary indexes should not ensures of future efficiency. Precise outcomes could differ materially from these expressed or implied. Previous efficiency just isn’t indicative of future outcomes. Traders ought to undertake their very own due diligence and thoroughly consider firms earlier than investing. ADVICE FROM A SECURITIES PROFESSIONAL IS STRONGLY ADVISED. © 2024. Nasdaq, Inc. All Rights Reserved.

{kind=link}