Betterment has a wide range of processes in place to assist restrict the affect of your investments in your tax invoice, relying in your scenario. Let’s demystify these highly effective methods.

We all know that the medley of account varieties could make it difficult so that you can determine which account to contribute to or withdraw from at any given time.

Let’s dive proper in to get an additional understanding of:

- What accounts can be found and why you would possibly select them

- The advantages of receiving dividends

- Betterment’s highly effective tax-sensitive options

How are completely different funding accounts taxed?

Taxable accounts

Taxable funding accounts are usually the simplest to arrange and have the least quantity of restrictions.

Though you may simply contribute and withdraw at any time from the account, there are trade-offs. A taxable account is funded with after-tax {dollars}, and any capital features you incur by promoting property, in addition to any dividends you obtain, are taxable on an annual foundation.

Whereas there is no such thing as a deferral of revenue like in a retirement plan, there are particular tax advantages solely out there in taxable accounts equivalent to decreased charges on long-term features, certified dividends, and municipal bond revenue.

Key Concerns

- You prefer to the choice to withdraw at any time with no IRS penalties.

- You already contributed the utmost quantity to all tax-advantaged retirement accounts.

Conventional accounts

Conventional accounts embody Conventional IRAs, Conventional 401(ok)s, Conventional 403(b)s, Conventional 457 Governmental Plans, and Conventional Thrift Financial savings Plans (TSPs).

Conventional funding accounts for retirement are typically funded with pre-tax {dollars}. The funding revenue obtained is deferred till the time of distribution from the plan. Assuming all of the contributions are funded with pre-tax {dollars}, the distributions are totally taxable as atypical revenue. For buyers beneath age 59.5, there could also be an extra 10% early withdrawal penalty except an exemption applies.

Key Concerns

- You anticipate your tax price to be decrease in retirement than it’s now.

- You acknowledge and settle for the potential for an early withdrawal penalty.

Roth accounts

This contains Roth IRAs, Roth 401(ok)s, Roth 403(b)s, Roth 457 Governmental Plans, and Roth Thrift Saving Plans (TSPs).

Roth sort funding accounts for retirement are all the time funded with after-tax {dollars}. Certified distributions are tax-free. For buyers beneath age 59.5, there could also be atypical revenue taxes on earnings and an extra 10% early withdrawal penalty on the earnings except an exemption applies.

Key issues

- You anticipate your tax price to be larger in retirement than it’s proper now.

- You anticipate your modified adjusted gross revenue (AGI) to be under $140k (or $208k submitting collectively).

- You want the choice to withdraw contributions with out being taxed.

- You acknowledge the potential for a penalty on earnings withdrawn early.

Past account sort selections, we additionally use your dividends to maintain your tax affect as small as attainable.

4 methods Betterment helps you restrict your tax affect

We use any extra money to rebalance your portfolio

When your account receives any money—whether or not by means of a dividend or deposit—we mechanically determine how you can use the cash that can assist you get again to your goal weighting for every asset class.

Dividends are your portion of an organization’s earnings. Not all corporations pay dividends, however as a Betterment investor, you virtually all the time obtain some as a result of your cash is invested throughout 1000’s of corporations on the planet.

Your dividends are a vital ingredient in our tax-efficient rebalancing course of. Once you obtain a dividend into your Betterment account, you aren’t solely getting cash as an investor—your portfolio can also be getting a fast micro-rebalance that goals to assist preserve your tax invoice down on the finish of the yr.

And, when market actions trigger your portfolio’s precise allocation to float away out of your goal allocation, we mechanically use any incoming dividends or deposits to purchase extra shares of the lagging a part of your portfolio.

This helps to get the portfolio again to its goal asset allocation with out having to unload shares. This can be a refined monetary planning approach that historically has solely been out there to bigger accounts, however our automation makes it attainable to do it with any dimension account.

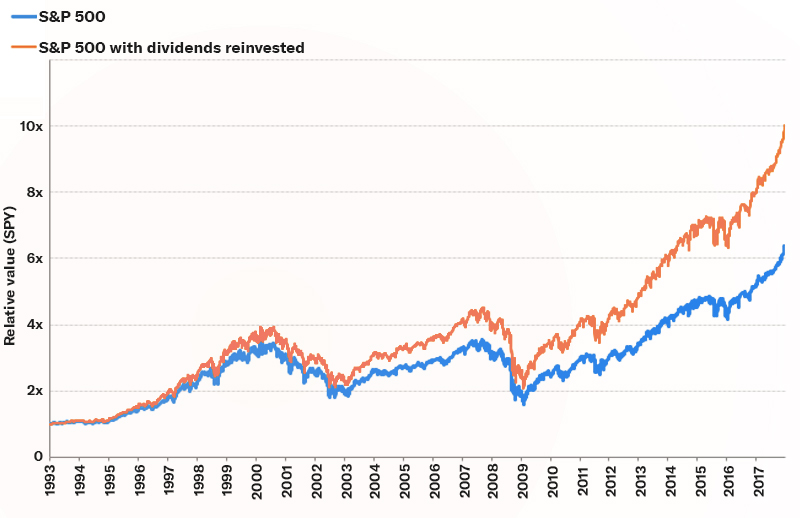

Efficiency of S&P 500 with dividends reinvested

Supply: Bloomberg. Efficiency is supplied for illustrative functions to characterize broad market returns for [asset classes] that is probably not utilized in all Betterment portfolios. The [asset class] efficiency is just not attributable to any precise Betterment portfolio nor does it replicate any particular Betterment efficiency. As such, it’s not internet of any administration charges. The efficiency of particular funds used for every asset class within the Betterment portfolio will differ from the efficiency of the broad market index returns mirrored right here. Previous efficiency is just not indicative of future outcomes. You can not make investments straight within the index. Content material is supposed for instructional functions and never meant to be taken as recommendation or a suggestion for any particular funding product or technique.

We “harvest” funding losses

Tax loss harvesting can decrease your tax invoice by “harvesting” funding losses for tax reporting functions whereas preserving you totally invested.

When promoting an funding that has elevated in worth, you’ll owe taxes on the features, often called capital features tax. Thankfully, the tax code considers your features and losses throughout all of your investments collectively when assessing capital features tax, which implies that any losses (even in different investments) will scale back your features and your tax invoice.

In truth, if losses outpace features in a tax yr, you may remove your capital features invoice fully. Any losses leftover can be utilized to cut back your taxable revenue by as much as $3,000. Lastly, any losses not used within the present tax yr could be carried over indefinitely to cut back capital features and taxable revenue in subsequent years.

So how do you do it?

When an funding drops under its preliminary worth—one thing that could be very more likely to occur to even one of the best funding in some unspecified time in the future throughout your funding horizon—you promote that funding to understand a loss for tax functions and purchase a associated funding to take care of your market publicity.

Ideally, you’ll purchase again the identical funding you simply bought. In spite of everything, you continue to assume it’s a very good funding. Nevertheless, IRS guidelines stop you from recognizing the tax loss should you purchase again the identical funding inside 30 days of the sale. So, with a view to preserve your total funding publicity, you purchase a associated however completely different funding. Consider promoting Coke inventory after which shopping for Pepsi inventory.

Total, tax loss harvesting might help decrease your tax invoice by recognizing losses whereas preserving your total market publicity. At Betterment, all it’s important to do is activate Tax Loss Harvesting+ in your account.

We use asset location to your benefit

Asset location is a technique the place you set your most tax-inefficient investments (normally bonds) right into a tax-efficient account (IRA or 401k) whereas sustaining your total portfolio combine.

For instance, an investor could also be saving for retirement in each an IRA and taxable account and has an total portfolio mixture of 60% shares and 40% bonds. As a substitute of holding a 60/40 combine in each accounts, an investor utilizing an asset location technique would put tax-inefficient bonds within the IRA and put extra tax-efficient shares within the taxable account.

In doing so, curiosity revenue from bonds—which is generally handled as atypical revenue and topic to the next tax price—is shielded from taxes within the IRA. In the meantime, certified dividends from shares within the taxable account are taxed at a decrease price, capital features tax charges as an alternative of atypical revenue tax charges. The whole portfolio nonetheless maintains the 60/40 combine, however the underlying accounts have moved property between one another to decrease the portfolio’s tax burden.

We use ETFs as an alternative of mutual funds

Have you ever ever paid capital achieve taxes on a mutual fund that was down over the yr? This irritating scenario occurs when the fund sells investments contained in the fund for a achieve, even when the general fund misplaced worth. IRS guidelines mandate that the tax on these features is handed by means of to the tip investor, you.

Whereas the identical rule applies to change traded funds (ETFs), the ETF fund construction makes such tax payments a lot much less probably. Normally, yow will discover ETFs with funding methods which might be related or equivalent to a mutual fund, usually with decrease charges.

{kind=link}